A few years back, insurance in India was something that most people would shun, including basic plans like the IPPB Group Accident Guard Policy. It was perceived as complex, costly, and hard to claim. People would rely solely on their savings or help from their family during an emergency.

Today, that would be a very risky practice. Accidents can occur at any point. Increasing medical expenses and the loss of income for a certain period after an injury could lead to long-term financial stress. Despite this, a large population still is without any form of accident cover.

This policy is designed to be:

- Low-cost

- Easy to access

- Simple to understand

But the real question is not what it is promising. The question is whether it actually offers substantial protection.

What Is the IPPB Group Accident Guard (GAG) Policy?

The Group Accident Guard (GAG) is a personal accident insurance plan offered to IPPB account holders.

What Makes It Different

Unlike traditional insurance:

- Focuses only on accidents, not illnesses

- It has low annual premiums

- It is distributed through post offices across India

Core Idea Behind the Policy

The policy is built for:

- Rural and semi-urban users

- First-time insurance buyers

People looking for basic financial protection often consider the IPPB Group Accident Guard Policy. It is not a complete insurance solution it is a risk buffer.

Key Features of the GAG Policy

Eligibility

Entry Age: 18 to 65 years (renewal able until around 80 years of age (depending upon plan))

Premium Options

The policy comes in multiple pricing tiers:

- ₹299

- ₹399

- ₹549 / ₹555

Each tier offers different coverage levels.

Sum Insured

Coverage typically ranges between:

- ₹5 lakh

- ₹10 lakh

Some higher variants may go beyond this

What This Means Practically

You pay a small yearly amount:

- In case of a serious accident, your family gets financial support

- Low cost does not mean low importance. It means limited but focused protection.

What Does the Policy Actually Cover?

Understanding what a policy like the IPPB Group Accident Guard Policy actually covers is more important than just knowing its price or benefits list. Many people buy insurance assuming it will help in all situations, but in reality, coverage is limited to specific conditions.

The Group Accident Guard policy focuses only on accident-related events and provides financial support in defined cases. To use this policy effectively, you need to clearly understand what is included, how each benefit works, and where the limitations are.

1. Accidental Death Benefit

If the policyholder dies due to an accident and 100% of the sum insured is paid to the nominee

Why This Matters

For many families the earning member is the only income source and this payout acts as immediate financial support.

2. Permanent Disability Coverage

What It Covers

- Loss of limbs

- Loss of eyesight

- Permanent physical disability

Why This Is Critical

Disability is often more financially damaging than death because:

- Income stops

- Expenses increase

3. Accidental Medical Expenses

- Coverage Includes

- Hospitalization (IPD)

- In some plans, OPD expenses

- Reality Check

- This is not full health insurance.

It only covers accident-related medical costs, not diseases.

4. Education Benefit

What It Offers

Financial support for up to 2 children

Why It Exists

If a parent dies or becomes disabled:

- Children’s education is often affected first

- This benefit tries to reduce that disruption.

5. Additional Benefits (Plan Dependent)

Some higher plans include:

- Daily hospital cash

- Funeral expenses

- Coma care

- Broken bone coverage

- Teleconsultation services

Important Note

These benefits sound attractive, but these actual payout amounts may be limited.

Premium Plans vs Basic Plans: What’s the Difference?

Basic Plan (₹299 – ₹355)

- Lower coverage (₹5-10 lakh)

- Limited medical expense coverage

- Fewer additional benefits

Suitable for:

- Entry-level users

- Those who want minimum protection

Premium Plan (₹399 – ₹555)

Higher and more structured benefits which includes education support and also a better hospitalization coverage

Suitable for:

- People with dependents

- Slightly higher risk protection needs

Key Insight

The difference in premium is small, but the difference in coverage can be meaningful.

What Is NOT Covered

This is where most people make mistakes.

The policy does NOT cover:

- Self-inflicted injury or suicide

- Accidents caused by alcohol or drugs

- Criminal activities

- Participation in riots Adventure activities

- e.g. bungee-jumping etc.

- Pre-existing health conditions

Why This Matters

Most claim rejections happen because people assume “everything is covered”, It is not.

How to Enroll in the GAG Policy

Process

- Visit a nearby post office

- Or contact an IPPB executive

- Must have an active IPPB account

What Makes It Simple

- Paperless process

- Minimal documentation

- Quick activation

Limitation

- Easy access can lead to

- Buying without understanding the policy

How the Claim Process Works

Step 1: Immediate Reporting

Inform the insurer (Tata AIG / Bajaj Allianz / Aditya Birla)

Step 2: Submit Documents

- FIR (for accidents)

- Medical reports

- Death certificate (if applicable)

- Policy details

Step 3: Claim Review

- Insurer verifies documents

- Processes payout

Key Reality

- Speed matters.

- Delayed reporting can:

- Reduce approval chances

- Complicate verification

Who Should Consider This Policy?

1. First-Time Insurance Buyers

- Low entry cost

- Easy to understand

2. Rural and Semi-Urban Users

- Accessible through post offices

- No need for online expertise

3. Individuals Without Any Insurance

Provides basic safety net

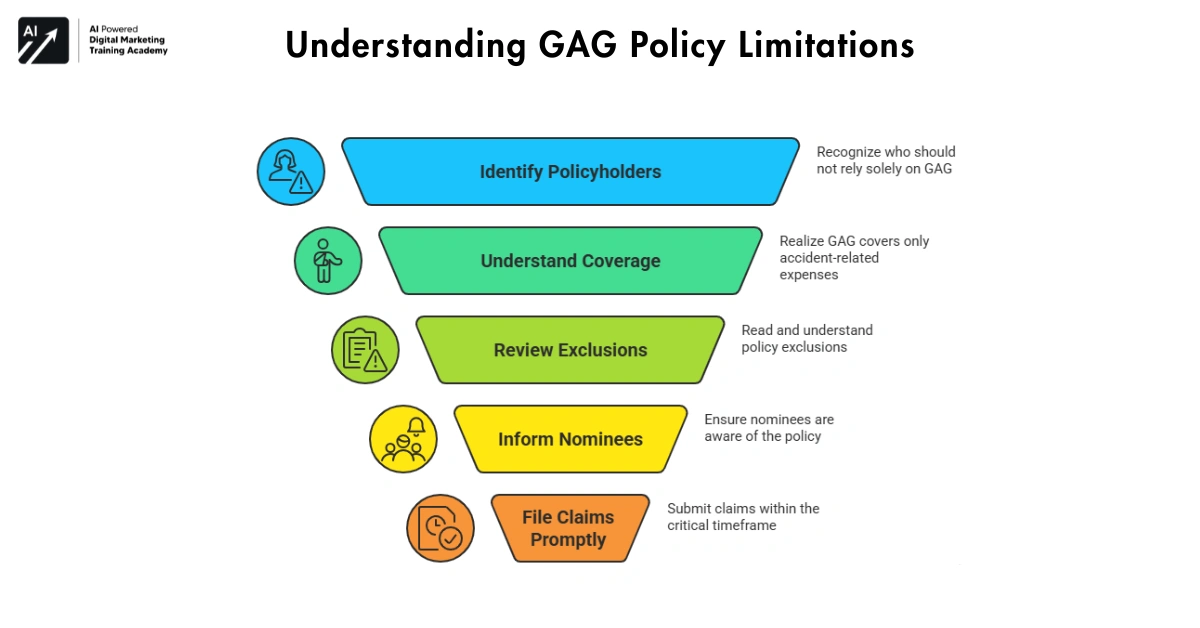

Who Should NOT Rely Only on This

People with families and high responsibilities and salaried individuals with higher income and anyone needing health coverage

This policy is not a replacement for:

- Health insurance

- Life insurance

1. Thinking It Covers All Medical Expenses

It does not. Only accident-related cases are covered.

2. Ignoring Exclusions

- Most people never read this section.

3. Not Informing Family Members

- If the nominee does not know:

- Claims may never be filed.

4. Delaying Claims

- Time is critical in accident cases.

Advantages of the GAG Policy

- Very low premium

- Easy enrollment

- Quick accessibility

- Focused accident protection

Limitations You Should Not Ignore

The policy has a limited coverage amount, which means the financial support may not be enough in serious situations. It also does not cover any illnesses, as it is strictly focused on accidents.

In addition, there are strict exclusions, so many common scenarios may not be eligible for claims if they fall outside the policy terms. Because of these limitations, it is not sufficient to rely on this policy alone for complete financial protection.

What Fund Houses and Insurers Gain From This

This is not purely a social product.

Business Perspective

- Expands insurance reach

- Targets untapped population

- Builds customer base

What This Means for You

Accessibility increases but responsibility shifts to you to understand the policy

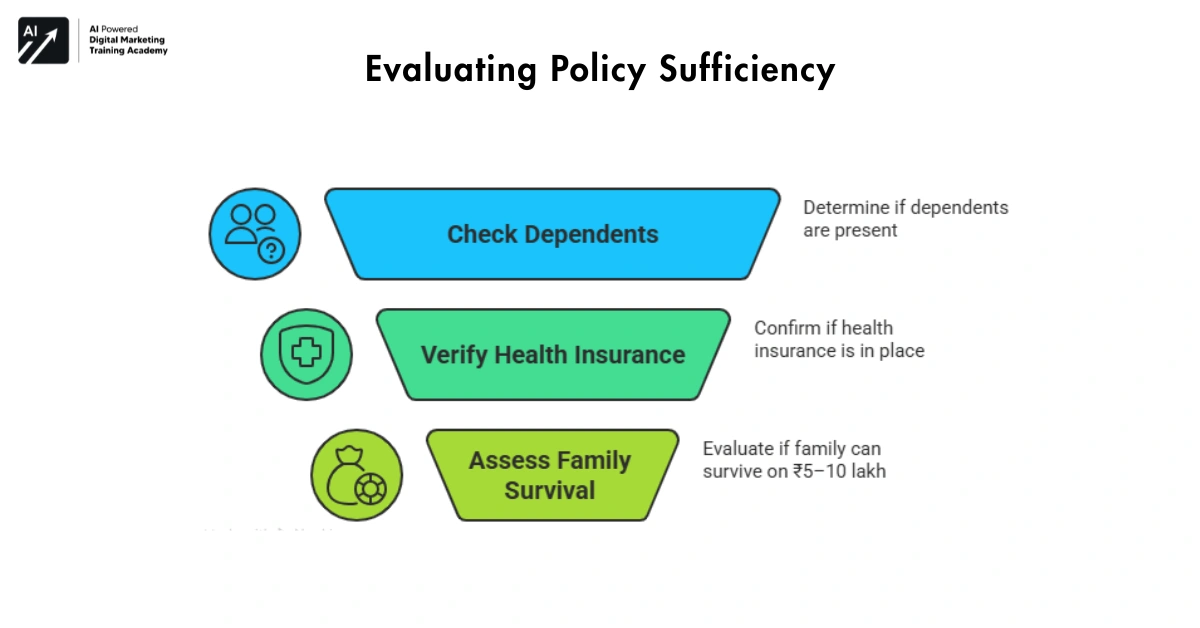

How to Evaluate If This Policy Is Enough for You

Ask yourself:

Do I have dependents?

- If yes → this alone is not enough

Do I have health insurance?

- If no → this does not replace it

Can my family survive on ₹5–10 lakh?

- If no → coverage is insufficient

- This policy is a support layer, not a full solution.

What You Should Do Before Buying

- Step 1: Read Key Benefits Clearly

- Step 2: Understand Exclusions

- Step 3: Compare Plan Variants

- Step 4: Inform Your Nominee

Real-Life Scenarios: When This Policy Actually Helps

Understanding a policy in theory is easy. The real clarity comes from situations.

Scenario 1: Road Accident with Hospitalization

- You meet with an accident and require hospitalization

- Medical bills are covered (within limits)

- This is where the policy works as expected.

Scenario 2: Permanent Disability

You lose the ability to work and the policy gives a payout and this helps, but ₹5 – 10 lakh may not sustain long-term income loss

Scenario 3: Death of Earning Member

- Family receives lump sum

- Useful for immediate expenses, but:

- Not enough for long-term financial stability

Scenario Where It Fails

- Illness (heart attack, cancer, etc.) → No coverage

- Injury under alcohol influence → Claim rejected

- Delay in reporting → Claim complications

Key Insight

This policy works for specific accident events, not for overall financial security.

How This Policy Fits Into a Complete Financial Plan

Most people make a structural mistake and they buy one policy and assume they are “covered” . That is incorrect.

A Basic Financial Protection Structure

A strong financial setup usually includes:

- Health Insurance

- Term Life Insurance

- Emergency Fund

- Accident Insurance (like GAG)

Where GAG Fits

It sits at the bottom layer and acts as an additional safety net

What Happens If You Skip Other Layers

If you only have GAG:

- No illness coverage

- No long-term income protection

- Limited financial backup

This creates a false sense of safety.

Correct Approach

Use GAG as:

- A starting point

- Or a supplementary cover

- Not as your main protection plan.

Key Questions to Ask Before Buying

Before purchasing, most people don’t ask the right questions.

They only look at:

- Price

- Coverage amount

- That is incomplete.

Ask These Instead:

What exact situations will trigger a claim?

- Not “accident” in general

- But specific condition

What situations will lead to rejection?

- Alcohol-related incidents

- Risky activities

Is the coverage enough for my family?

- ₹5 – 10 lakh sounds large

- But may not last long

Who will claim if something happens to me?

Does your nominee know the process?

Do I already have overlapping coverage?

Some employers provide accident insurance

Why This Matters

These questions:

- Reduce misunderstanding

- Prevent wrong expectations

- Improve decision quality

Final Thoughts

The IPPB GAG policy solves an important problem: lack of basic accident protection.

It makes insurance:

- Affordable

- Accessible

- Simple

But simplicity can also be misleading.

This policy is useful if:

- You understand its limits

- You use it as an additional layer

It becomes dangerous if:

- You depend on it completely

- You assume it covers everything

In financial planning, the biggest mistake is not the lack of products. It is false confidence in incomplete protection especially when relying only on the IPPB Group Accident Guard Policy and that is exactly what you need to avoid.

{kind=link}