From April 1 2026 the PAN card rules are going to change a lot on how financial transactions are monitored in India. These updates affect cash deposits, property deals, vehicle purchases, insurance policies and even event spending.

Most people only notice these rules when a transaction gets blocked or delayed. By then, the cost is time, penalties, or tax scrutiny. This guide explains what is changing, why it matters, and what you should do to stay compliant.

What Changes from April 1?

The new rules shift the focus from individual transactions to overall financial behavior.

Key highlights in simple terms

- Annual tracking replaces per-transaction limits

- Multiple accounts are monitored together

- Some thresholds are increased

- Some requirements are stricter (full traceability)

Why these rules are changing

The government aims to:

- improve financial transparency

- reduce unreported income

- track high-value activity more effectively

Instead of checking one transaction at a time, authorities now evaluate your total financial pattern.

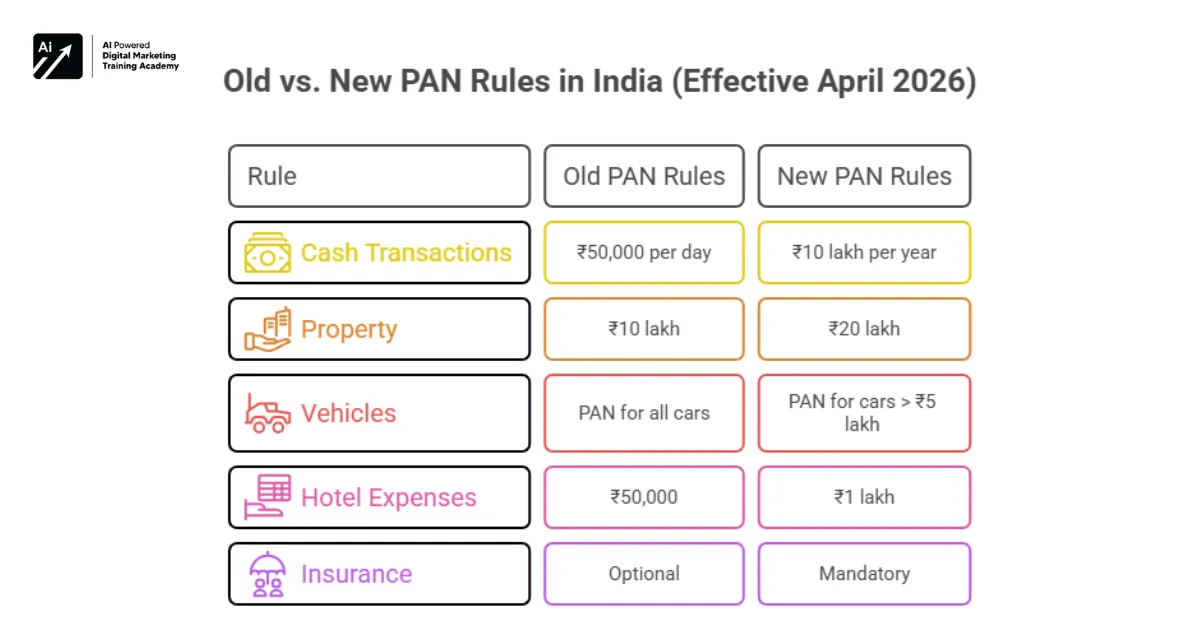

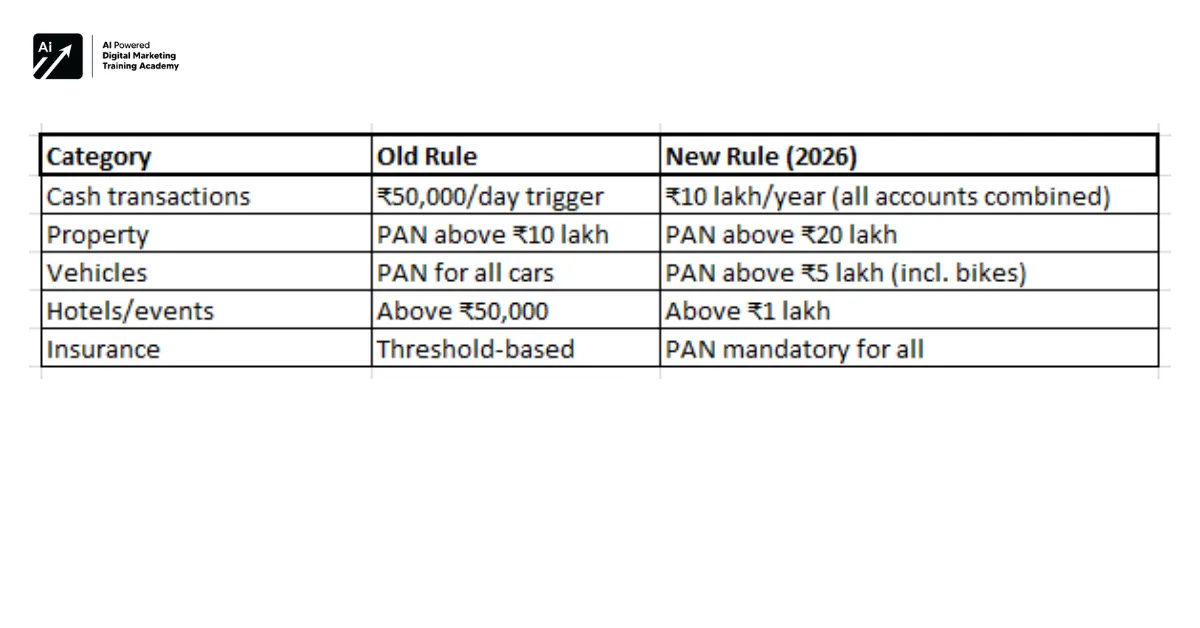

Quick Summary of PAN Rule Changes (2026)

Transactions where PAN is required

-

cash deposits/withdrawals above ₹10 lakh annually

-

property deals above ₹20 lakh

-

vehicle purchases above ₹5 lakh

-

hotel/event spending above ₹1 lakh

-

any new insurance policy

How PAN Tracking Works in 2026 (New System Explained)

The biggest change is how transactions are monitored.

![]()

Simple workflow:

- You make transactions (cash, property, purchases)

- Banks and institutions aggregate your activity

- Data is reported via SFT (Statement of Financial Transactions)

- Income Tax systems analyze patterns

Key insight

Splitting transactions or using multiple accounts no longer avoids detection.

Rule 1 – PAN for Cash Transactions Above ₹10 Lakh

This is the most impactful update because it targets cash behavior directly.

Old vs new rule explained

- Earlier: PAN required per transaction above ₹50,000

- Now: PAN required if total cash activity exceeds ₹10 lakh annually

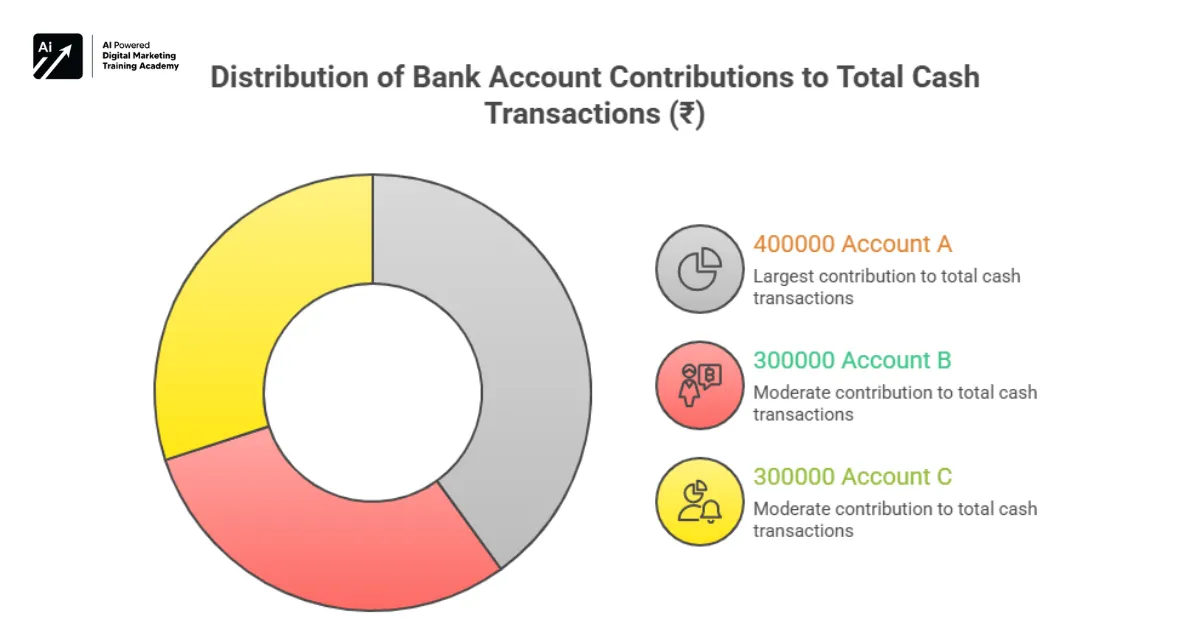

How annual tracking across accounts works

All your bank accounts are combined into one view. The system tracks your total deposits and withdrawals.

Scenarios

Example 1: Multi-account usage

- ₹4 lakh in Bank A

- ₹3 lakh in Bank B

- ₹3 lakh withdrawal

Total = ₹10 lakh → PAN required

Example 2: Spread over time

- ₹2 lakh deposited every quarter

Total = ₹8 lakh

Later ₹3 lakh withdrawal → total ₹11 lakh → PAN required

Who is most affected

- small businesses dealing in cash

- traders and freelancers

- individuals managing multiple accounts

Rule 2 – PAN for Property Transactions Above ₹20 Lakh

This rule introduces both relaxation and wider coverage.

What transactions are covered

- purchase

- sale

- gift

- joint development agreements

Old vs new comparison

- Old: PAN required above ₹10 lakh

- New: PAN required above ₹20 lakh

Scenarios

Example 1: Lower-value property

- ₹18 lakh purchase → PAN not required

Example 2: Non-cash transfer

- ₹25 lakh property gifted → PAN required

Practical insight

Even if no money is exchanged, ownership value triggers compliance.

Rule 3 – PAN for Vehicle Purchases Above ₹5 Lakh

This rule targets high-value vehicle purchases more precisely.

Changes for cars and bikes

- Vehicles below ₹5 lakh → PAN not required

- Vehicles above ₹5 lakh → PAN required

- Two-wheelers included for the first time

Scenarios

Example 1: Budget car

- ₹4.7 lakh → no PAN required

Example 2: Premium bike

- ₹6 lakh → PAN required

Key takeaway

Compliance is now linked to value, not vehicle type.

Rule 4 – PAN for Hotel Bills and Event Spending

This rule increases the threshold, reducing compliance for smaller expenses.

Updated threshold

- Old: ₹50,000

- New: ₹1 lakh

What counts as event spending

- weddings

- banquet bookings

- corporate events

Scenarios

Example 1: Family dinner

- ₹60,000 → no PAN required

Example 2: Wedding booking

- ₹2 lakh → PAN required

Important note

Businesses may still report aggregated spending even if payments are split.

Rule 5 – PAN Mandatory for All Insurance Policies

This is one of the strictest changes.

What changed

- Earlier: PAN required only above certain premium

- Now: PAN required for every policy

Scenarios

Example 1: Small policy

- ₹5,000 premium → PAN required

Example 2: Large policy

- ₹75,000 premium → PAN required

Why this matters

Insurance is now fully linked to your financial identity, improving traceability.

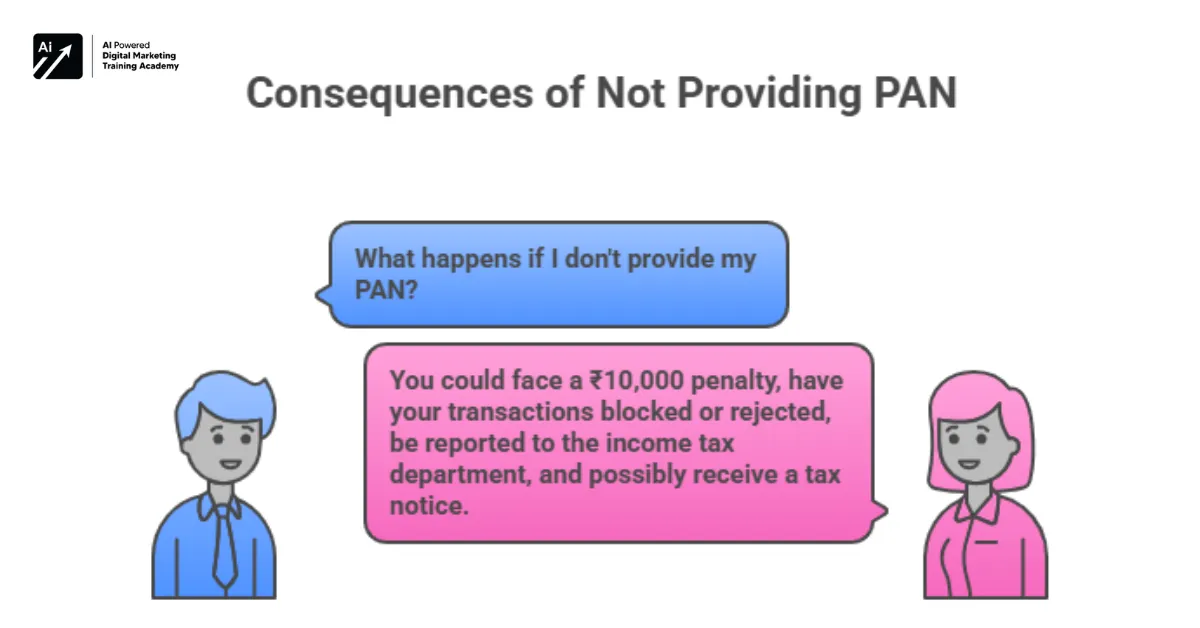

What happens if PAN not provided?

Ignoring PAN requirements leads to immediate and long-term consequences.

Penalty under Section 272B

- ₹10,000 per instance

Transaction-level impact

- bank may reject deposits

- registrar may stop property registration

System-level impact

- transaction reported under SFT

- mismatch triggers tax scrutiny

Worst-case scenario

- transaction blocked

- reported to Income Tax Department

- notice issued for unexplained income

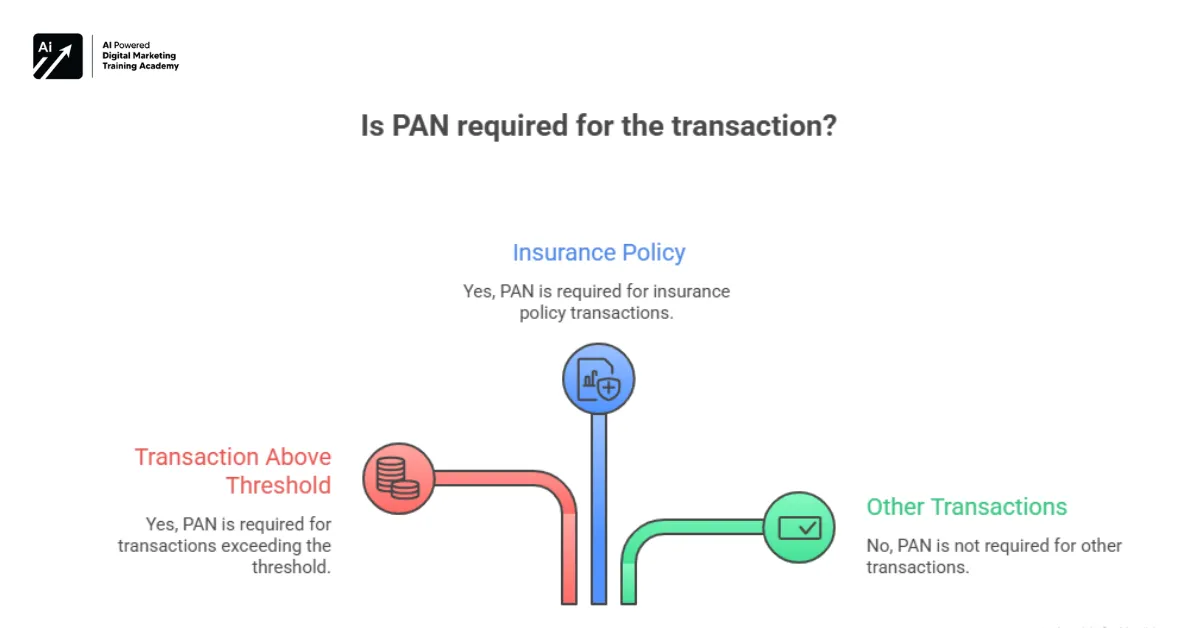

Transactions Where PAN Is Mandatory in 2026

You must provide PAN if:

- total cash transactions exceed ₹10 lakh annually

- property value exceeds ₹20 lakh

- vehicle price exceeds ₹5 lakh

- event or hotel spending exceeds ₹1 lakh

- you purchase any insurance policy

Common mistakes to Avoid

Splitting transactions

Breaking payments into smaller parts no longer works due to aggregation.

Using multiple bank accounts

All accounts are tracked together, removing this loophole.

Ignoring PAN linkage

Unlinked PAN can result in rejected or delayed transactions.

Misunderstanding thresholds

Some limits increased (property), while others were removed (insurance).

Do You Need PAN? (Quick Decision Framework)

Use this simple logic:

- Is your transaction above the defined threshold?

- Is your total annual activity crossing limits?

- Are you buying insurance?

If yes to any → PAN must be provided.

What You Should Do Now (Compliance Checklist)

Update PAN everywhere

Link PAN to:

-

bank accounts

-

insurance

-

investments

Track annual financial activity

Focus on total cash movement across all accounts, not just single transactions.

Prepare ahead of high-value transactions

Make sure PAN is ready before:

- property deals

- vehicle purchases

- event bookings

It is very important to keep income and the money spend in balance.

difference may trigger scrutiny.

Why the Government is tightening PAN rules

These updates show move towards data-driven tax systems make better.

Financial transparency

Authorities now rely on:

- centralized reporting

- behavioral analysis

Reducing tax evasion

By tracking activity can remove common loopholes. This helps to make things fair for everyone because total activity is being watched closely.

FAQs

What are the new PAN rules from April 2026?

The new rules require PAN for high value cash transactions above ₹10 lakh in a year, property deals above ₹20 lakh, vehicle costs above ₹5 lakh and all insurance policies. The system now tracks cumulative financial activity not only individual transactions.

Is PAN mandatory for cash deposits in 2026?

Yes. If cash deposits or withdrawals are more than ₹10 lakh in a financial year across all accounts. Even if individual transactions are small, cumulative tracking applies.

What is the penalty for not providing PAN?

If you do not provide PAN when required, it might lead to ₹10,000 penalty per instance under Section 272B. Additionally, to that transactions may be rejected or reported for further review.

Is PAN required for buying a bike?

Yes. If price is over ₹5 lakh. Bikes below this threshold are exempt under the new rules.

Can splitting transactions avoid PAN rules?

No. Transactions are now tracked cumulatively across accounts. Splitting payments or using multiple banks will not bypass PAN requirements.

Conclusion

The PAN card new rules 2026 shift compliance from transaction-level checks to full financial visibility.

To stay compliant:

- monitor total financial activity

- ensure PAN is linked across accounts

- track high-value transactions

These rules are made to stop people from finding loopholes. If adapting to these new rules early will help to avoid disruptions, penalties and unnecessary scrutiny.

{kind=link}