Every startup begins with hope an idea, a small team, and a big dream. This is your guide on “How to Legally Start a Startup in India.” At this stage, founders think about customers, growth, and money.

Legal work feels slow and boring. Legal registration is not just paperwork. It is the base of your startup, When a startup is not legally registered, the law does not see it as a business. It sees it as a person. That person is you. This means if something goes wrong, you are personally responsible.

Why Legal Registration Is Important for Startups in India

India has clear business laws. If you earn money without registration, the government can question you. Many founders receive notices not because they did something wrong, but because they didn’t register on time. These notices create fear and confusion.

Once your startup is legally registered:

- Your business follows the law

- Your income is tracked properly

- You avoid penalties and fines

Legal clarity removes stress.Stress-free founders think better.

Build trust with investors and banks

No investor funds an unregistered startup. No bank opens an account without documents.

Even clients today check:

- Company name

- GST number

- Registration proof

A registered startup looks serious. An unregistered one looks risky. Trust is invisible, but it decides growth.

Access tax benefits and government schemes

India supports startups strongly. But only registered startups get benefits.

Once registered, you can apply for:

- Startup India benefits

- DPIIT recognition

- Tax exemption under Section 80-IAC

These benefits save money. Saved money gives startups time to grow.

So when you learn how to legally start a startup in India, you are not just following rules.

You are building a safe future.

In short:

- Registration protects you

- Registration builds trust

- Registration unlocks growth

Now that the “why” is clear, let’s move to the “how”.

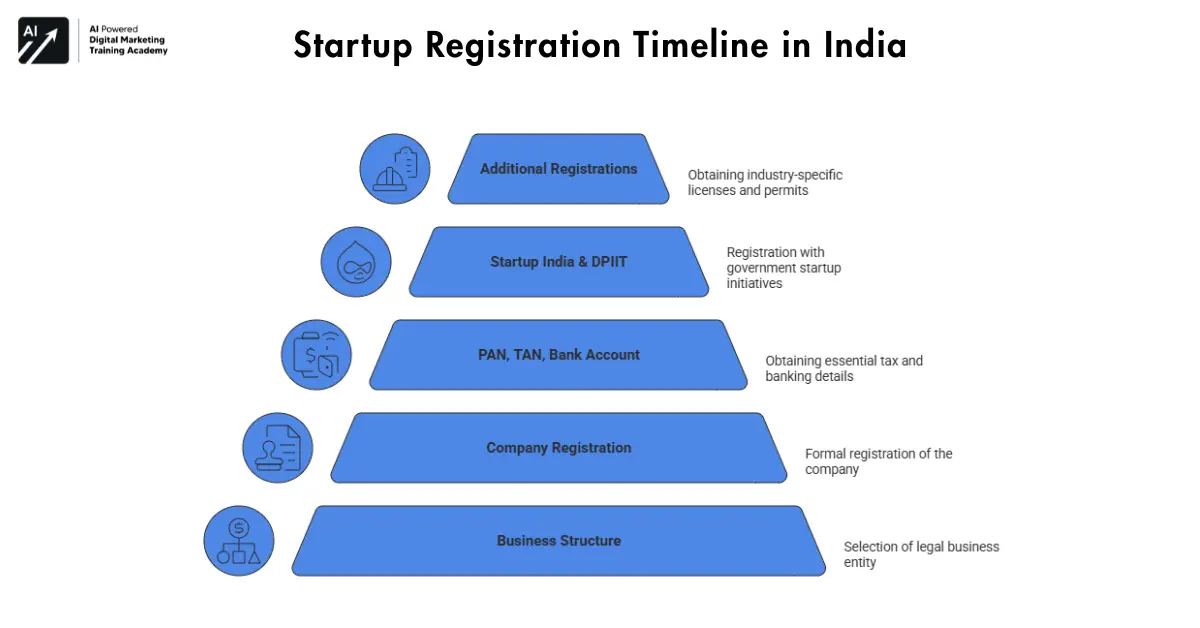

Step 1 : Choose the Right Business Structure for Your Startup

Before registering your startup, you must make one important decision. You must choose the business structure.

This decision decides:

- Your risk level

- Your tax system

- Your future growth

Many beginners skip this step.They copy what others choose. This creates problems later. A business structure is like the bones of your startup. If bones are weak, growth hurts.

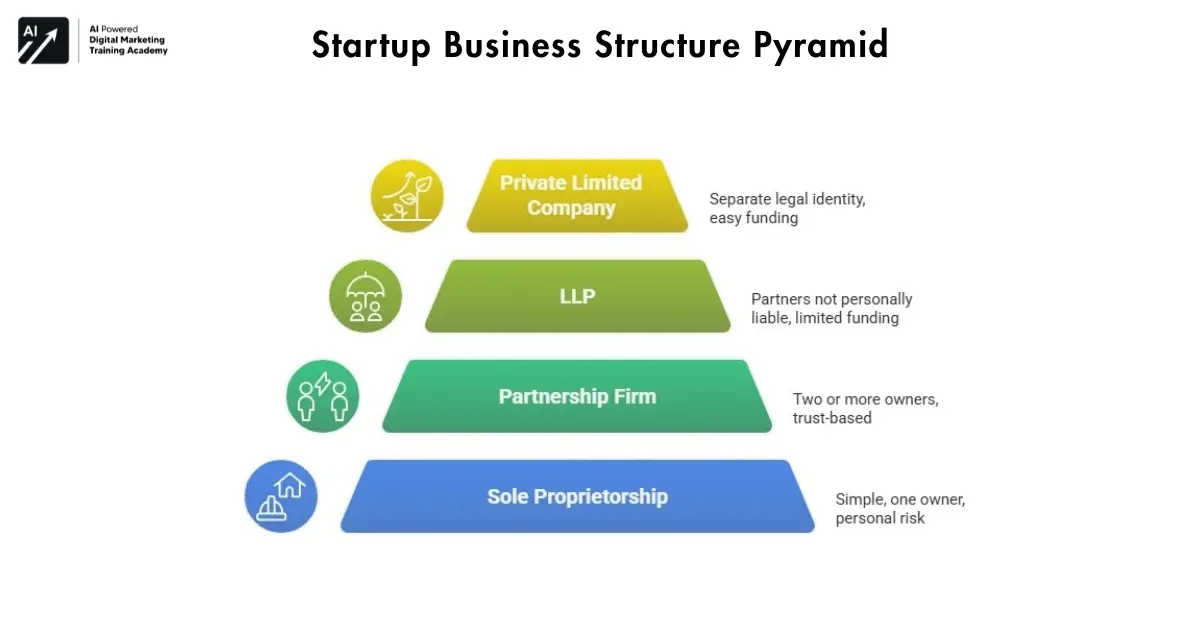

Types of Business Structures in India to Legally Start a Startup

India offers four common business structures. A Sole Proprietorship is the simplest. One owner. Easy setup. But there is no separation between owner and business. If the business fails, your personal money is at risk. A Partnership Firm has two or more owners. It works when trust is strong. But disputes can destroy businesses.

An LLP (Limited Liability Partnership) gives protection to partners. Partners are not personally liable. However, funding options are limited. A Private Limited Company is the most preferred choice for startups. It is built for growth.

Which Business Structure Is Best for Startups?

For most startups, Private Limited Company is the best option.

Because it gives:

- Separate legal identity

- Limited liability

- Easy funding

- Better credibility

Investors trust private limited companies. Banks prefer them. Government schemes support them.

Here is a simple comparison idea:

- Sole proprietorship = easy but risky

- Partnership = shared but unstable

- LLP = safe but limited

- Private limited = safe and scalable

If your goal is:

- Raising funds

- Hiring teams

- Scaling nationally

Private limited is the right choice. Choosing the correct structure early saves years of trouble. Once this is done, registration becomes smooth.

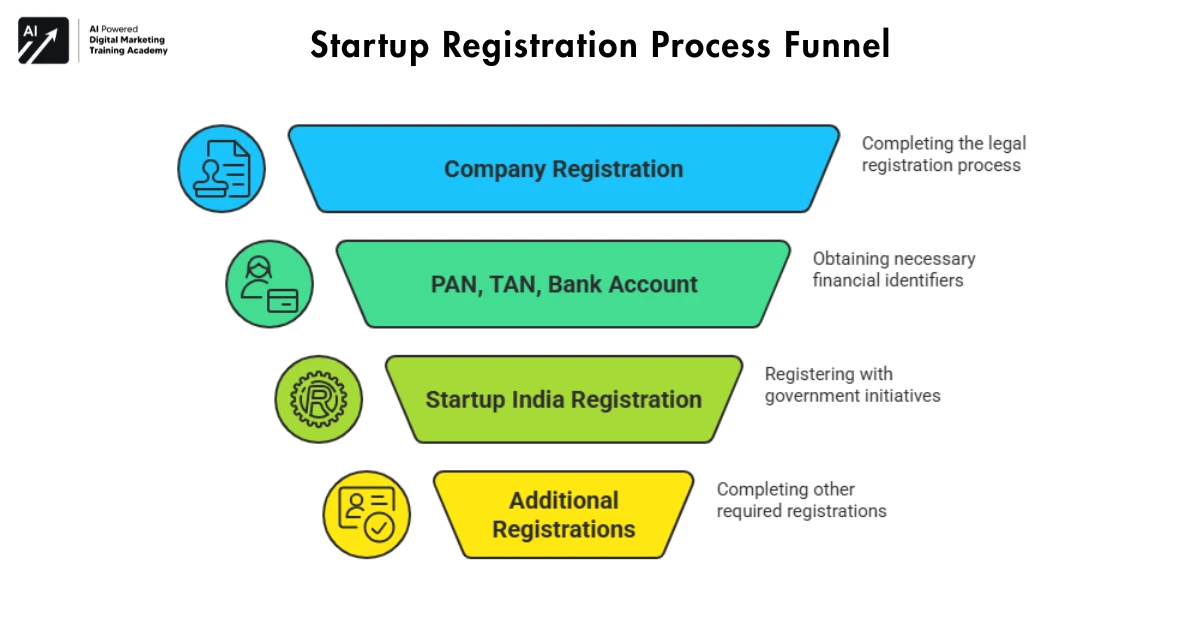

Step 2 : Company Registration Process in India

Now comes the step where your startup becomes real. Company registration in India looks complex online. But in reality, it is a clean step-by-step process. No legal background and no heavy English needed.

Documents Required for Company Registration

You only need basic documents:

- PAN card

- Aadhaar card

- Address proof

- Email ID and phone number

Steps to Register a Private Limited Company

First, you need to apply for a Digital Signature Certificate which is also called DSC. This works like your online signature. Next, you get a Director Identification Number (DIN). Every director must have this number.

Then you apply for company name approval through the MCA portal. The name must be unique and meaningful. After name approval, you file the SPICe+ form.

This form handles:

- Incorporation

- PAN

- TAN

Once you got approval, you receive:

- Company Registration Certificate

- Company PAN

- Company TAN

This will take 7 to 10 working days of process. That day feels special. Your idea officially becomes a company. And just like that, your startup enters the legal world.

Step 3 : Apply for PAN, TAN & Open a Company Bank Account

Once your company is registered, many founders feel relieved. They think the hard work is done. But this step is just as important as registration. PAN, TAN, and a company bank account are the financial backbone of your startup. Without them, your business cannot operate legally. Let’s understand this in a simple way.

Why PAN and TAN matter for startups

A PAN (Permanent Account Number) is like your company’s identity for taxes. Every rupee your startup earns or spends is linked to PAN.

A TAN (Tax Deduction and Collection Account Number) is used when your startup deducts tax. For example, when you pay salary or professional fees.

Without PAN and TAN:

- You cannot file taxes

- You cannot comply with government rules

- You may receive penalties

The good news is, when you register a private limited company, PAN and TAN are issued automatically through the SPICe+ form. Still, you must understand their importance.

PAN helps the government track:

- Income

- Expenses

- Profit

TAN helps track:

- TDS deductions

- Salary payments

- Professional fees

Ignoring these creates trouble later.

Why opening a company bank account is important

Now comes the most ignored step by beginners. Opening a current bank account in the company name. Many founders continue using their personal account. This is a big mistake.

A company bank account creates a clear line between personal money and business money. This clarity saves time, stress, and confusion.

Benefits of a company bank account

- Keeps personal and business money separate

- Required for GST and compliance

- Builds trust with clients and vendors

- Makes accounting easy

Banks ask for:

- Company Registration Certificate

- Company PAN

- Address proof

- Director KYC

Once approved, your startup becomes financially active.

You can now:

- Receive client payments

- Pay vendors

- Track expenses properly

Think of this step as opening the front door of your business. Without it, everything stays stuck. Many legal problems in startups come from mixed finances. Avoid this mistake early.

Once PAN, TAN, and bank accounts are ready, your startup is not just registered, it is operational. Now let’s move to a step that many founders ignore, but later regret.

Step 4 : Startup India Registration & DPIIT Recognition

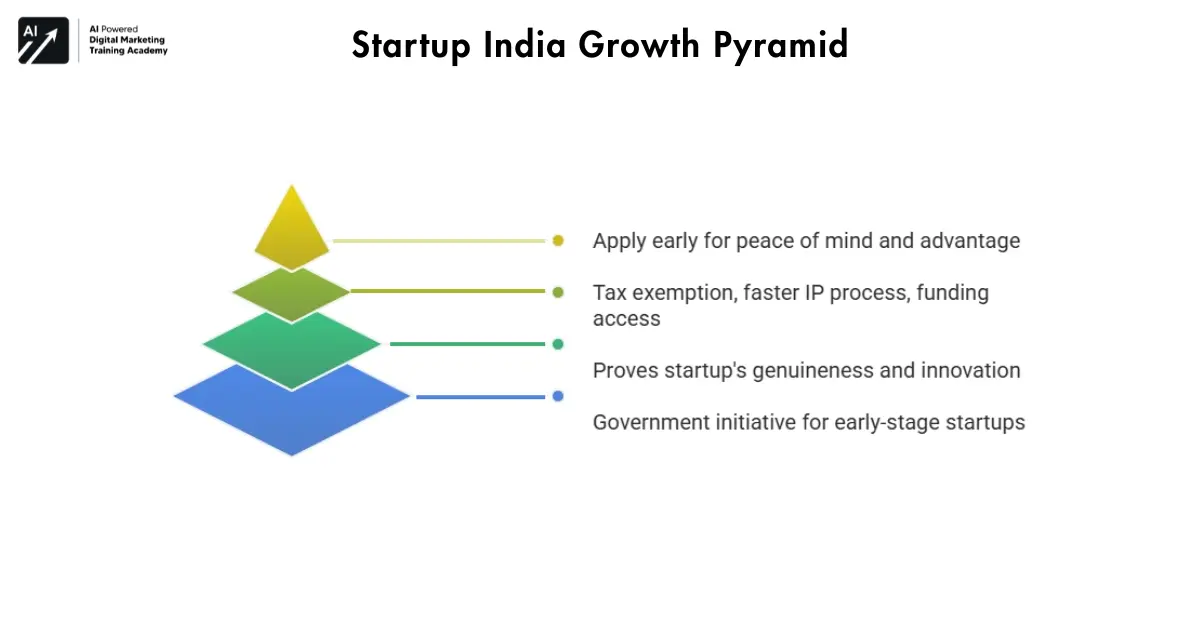

India wants startups to grow. That is why the government created Startup India. Yet, many founders don’t register. Not because it is hard, but because no one explains it simply. Let’s fix that.

Startup India Government Registration for Startups

This startup India is a government initiative that supports early-stage startups. Registration is done on the Startup India portal. It takes very little time. Once registered, you can apply for DPIIT recognition.

This recognition proves that:

- Your startup is genuine

- Your business is innovative

- You are eligible for benefits

Startup India registration does not replace company registration. It works after your company is formed. Just think this is an extra layer of support.

Why DPIIT recognition matters

Many founders think this is optional. Technically, yes. But practically, it is powerful.

With DPIIT recognition, your startup becomes visible to the government ecosystem.

Benefits of DPIIT recognition

- Tax exemption under Section 80-IAC

- Faster trademark and patent process

- Access to government grants and funding

- Better credibility with investors

Let’s talk about tax benefits. Under Section 80-IAC, eligible startups can enjoy tax exemption for three consecutive years. This saves lakhs of rupees.

That saved money can be used for:

- Hiring

- Marketing

- Product development

DPIIT recognition also helps with IPR benefits. Trademark and patent filings become faster and more affordable, which protects your brand at an early stage. When you understand how to legally start a startup in India, DPIIT recognition also opens doors to funding. Many government schemes and startup incubators require DPIIT recognition, and without it, your startup is not eligible.

Simple mindset shift

Founders often delay this step. They think they will apply “later”. But later often never becomes.

Applying early gives:

- Peace of mind

- Financial advantage

- Legal clarity

Startup India registration is not about today. It is about preparing for tomorrow. Once this step is done, your startup stands on strong legal ground.

Step 5 : Mandatory Registrations After Company Formation

Once your company is registered and your bank account is active, many founders feel they are done. But this is where most beginners slow down or stop. Company formation is just the entry gate. Mandatory registrations are the safety locks.

These registrations depend on:

- Your business type

- Your turnover

- Your operations

Ignoring them may not cause trouble today, but it always may create problems later. Let’s go step by step.

GST Registration – Who Needs It?

GST is one of the most confusing topics for new founders. People hear many opinions and feel scared.So let’s keep it simple. GST (Goods and Services Tax) is required only in certain cases.

You must register for GST if:

- Your turnover crosses the limit

- You sell on online platforms

- You do inter-state business

For most startups:

- Service businesses → GST required after ₹20 lakh

- Product businesses → GST required after ₹40 lakh

However, some startups need GST from day one, even with zero revenue.

Why GST registration matters

- Makes your business legally compliant

- Required to work with big clients

- Allows you to claim input tax credit

Many startups delay GST and later face:

- Notices

- Penalties

- Payment blocks

If you plan to grow, GST registration is not optional, it is preparation.

Shops & Establishment License

This registration is often ignored. But it is important. The Shops & Establishment License proves that your office exists legally.

Even if:

- You work from home

- You have a small office

- You have a co-working space

This license may still apply.

It is issued by the state government and covers:

- Working hours

- Employee rights

- Office compliance

Why this license is required

- Needed for inspections

- Required for bank and vendor verification

- Shows legal presence

Think of it as your office’s legal ID.

MSME (Udyam) Registration

MSME registration is free, simple, and powerful. Yet many founders skip it.

MSME registration puts your startup under the “Udyam portal” and classifies it as:

- Micro

- Small

- Medium enterprise

Benefits of MSME registration

- Easy access to loans

- Lower interest rates

- Financial help from the government

- Priority in tenders

This registration also builds credibility with banks. If your startup is eligible, this is a must-do step.

Trademark Registration

Your brand is your identity. Your name, logo, and tagline matter. Trademark registration protects this identity.

Without trademark:

- Anyone can copy your name

- You may lose brand rights later

Many startups register trademarks after building popularity. This is risky.

Why trademark protection matters

- Secures brand ownership

- Builds investor confidence

- Prevents legal disputes

Trademark registration is optional early on, but very important for long-term growth.

Key takeaway from Step 5

Mandatory registrations may feel boring. But they protect your startup silently. These steps don’t create revenue. They protect revenue.

Founders who complete these early:

- Face fewer notices

- Gain trust faster

- Grow smoothly

Now that your startup is fully registered and compliant, let’s look at mistakes founders make so you don’t repeat them.

Common Legal Mistakes New Startup Founders Make

Most startup failures do not happen because of bad ideas. They happen because of small legal mistakes made early. These mistakes look harmless in the beginning. But later they grow into serious problems. Let’s talk about the most common things so you can avoid them.

Delaying legal registration

Many founders start earning before registering. They think registration can wait. This delay creates risk.

When income starts flowing without registration:

- Taxes become messy

- Notices may arrive

- Compliance becomes confusing

Later, fixing these mistakes costs more money and time. Early registration brings clarity. Clarity brings confidence.

Choosing the Wrong Business Structure Can Hurt Your Startup

Some founders choose sole proprietorship because it is easy. Others choose partnership because friends suggested it. But when learning how to legally start a startup in India, ease today can cause pain tomorrow.

Wrong structure leads to:

- Personal liability

- Funding rejection

- Legal restructuring later

Changing structure later is costly. Choosing right at the start saves years of effort.

Ignoring GST and compliance

Many startups ignore GST because revenue is low.They think compliance is for big companies.

But GST rules apply based on:

- Business type

- Location

- Client requirements

Ignoring GST leads to:

- Penalties

- Blocked payments

- Loss of clients

Compliance is not punishment. It is protection.

A Common Legal Mistake in Indian Startups

This mistake looks small. But it causes huge confusion.

Using personal accounts for business:

- Breaks accounting

- Creates tax issues

- Raises audit risk

A separate bank account keeps things clean.

Key lesson

Most legal mistakes come from lack of guidance, not intention. Smart founders learn early. They build legally before they grow financially.

Cost to Legally Start a Startup in India

Cost is one of the biggest fears for beginners. Many think legal registration is expensive. The truth is different. Starting a startup legally in India is affordable when done correctly. Let’s break this down simply.

Government fees vs professional fees

Government fees are fixed. Professional fees vary.

Government costs include:

- Name approval

- Incorporation charges

Professional fees include:

- Consultation

- Filing support

- Compliance guidance

Approximate cost breakdown

For a private limited company:

- Government fees: low to moderate

- Professional help: optional but useful

The total cost depends on:

- Number of directors

- Capital

- State

Most startups can legally start within a reasonable budget.

Hidden cost of not registering

Not registering also has a cost.

That cost includes:

- Penalties

- Legal notices

- Missed funding opportunities

Skipping legal steps to save money often leads to bigger losses later. Smart mindset Legal cost is not an expense.It is an investment.

An investment that protects:

- Your money

- Your brand

- Your future

Founders who plan legally spend less overall.

Timeline: How Long Does It Take to Register a Startup in India?

Time matters in startups. Founders want to move fast. The good news is that legal registration in India is not slow. When documents are ready, the process is smooth and efficient.

Realistic Registration Timeline to Legally Start a Startup in India

Here is a simple view.

Business structure selection:

- 1 to 2 days

Company registration process:

- 7 to 10 working days

PAN, TAN, and bank account:

- 5 to 7 days

Startup India & DPIIT registration:

- 1 to 2 days

Additional registrations (GST, MSME, etc.):

- Depends on business type

What Causes Delays When You Legally Start a Startup in India

Delays usually happen because of:

- Incorrect documents

- Name rejection

- Incomplete information

Planning early reduces delays.

Why speed matters

Fast legal setup helps you:

- Start billing early

- Apply for funding

- Build trust faster

Legal speed supports business speed.

Conclusion: From Idea to Legally Registered Startup

Every startup starts with a dream. But only some dreams survive. The difference is not talent. It is legal clarity.

Founders who register legally:

- Sleep better

- Grow faster

- Face fewer surprises

This guide showed you how to legally start a startup in India, step by step, without fear or jargon. Legal work is not boring. It is empowering.

When your startup is legal:

- You feel confident

- You earn trust

- You build long-term value

Straight from the courtroom to your boardroom.

{kind=link}